Maintaining a healthy credit profile is often a balancing act, but one specific factor carries more weight than any other. If you are looking to secure a loan or a new credit card, understanding this "silent killer" is the first step toward financial stability.

The Heavyweight Champion of Credit Scoring

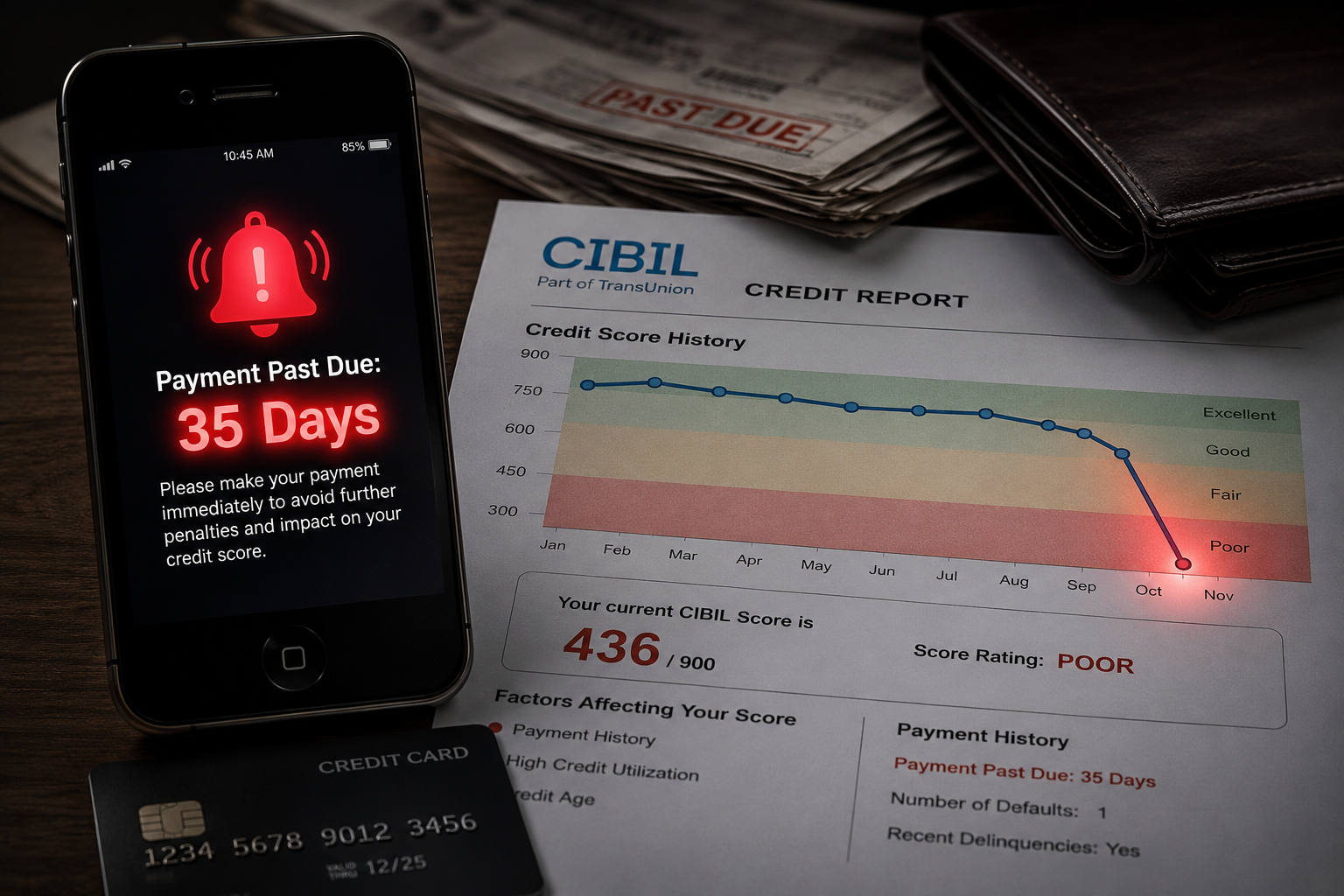

While many people worry about checking their score too often or closing old accounts, the single biggest factor affecting your credit is Payment History. In most scoring models, including CIBIL, your track record of on-time payments accounts for approximately 35% of your total score.

A single payment that is more than 30 days overdue can cause a significant and immediate drop. This is because lenders view past behavior as the most reliable predictor of future risk. One missed cycle suggests financial instability, making you appear as a high-risk borrower.

The Secondary Threat: Credit Utilization

Close behind payment history is Credit Utilization Ratio. This refers to how much of your available credit limit you are actually using. Even if you pay your bills on time, keeping your credit card balances near their limits—typically above 30%—signals to lenders that you are overextended. This can "choke" your score, preventing it from reaching its full potential.

Strategic Ways to Protect Your Profile

To keep your credit health in peak condition, consider these proactive steps:

Automate Your Deadlines: Set up standing instructions or auto-debits for at least the minimum amount due to ensure you never miss a date.

Monitor Your DPD: Regularly check your reports for "Days Past Due" (DPD) entries. Even small errors in reporting can be rectified if caught early.